Stripe: Becoming the Financial Heartbeat of Small Businesses

By: Marcus Shen & Claire Ku

The Ivey Business Review is a student publication conceived, designed and managed by Honors Business Administration students at the Ivey Business School.

The Pulse Check: Stripe’s Small Business Segment

Today, Stripe processes $1.4 trillion in payments a year for merchants, many of which are small businesses. From indie developers launching their first app to e-commerce shops selling candles, Stripe has made collecting money effortless, but spending and managing finances are still disjointed.

On average, small businesses use ten different digital tools to manage their financial operations and overspend by roughly $3,000 a month on software they rarely use. This highlights the fragmented nature of the accounting and financial management market.

On one end, enterprise platforms such as NetSuite and SAP exist, which are too complex and expensive for most small businesses. On the other end are legacy platforms like QuickBooks, Xero, and FreshBooks. QuickBooks has become the default bookkeeping system for small businesses, holding 75 percent of the US accounting software market. Despite their dominance and some integration features with Stripe, these accounting platforms remain one step removed from the revenue-generating side of businesses.

56 percent of small businesses report difficulty paying operating expenses correctly, and 51 percent struggle with unpredictable cash flows. In fact, cash flow problems account for 82 percent of small business failures because businesses lack a simple way to manage their finances. Stripe, which already sits at the center of how small businesses collect revenue, is uniquely positioned to solve this. This can be done not by building out another standalone tool, rather by connecting the dots.

Introducing: Pulse by Stripe, Real-Time Financial Health Management

Stripe is well-positioned to solve this challenge by introducing Pulse, a platform that brings revenue collection and expense management together. It allows businesses to manage all aspects of their finances, including payables, receivables, closing the books, taxes, and financial planning, in one place. For founders who are focused on operating their business, Pulse fills the CFO gap with minimal friction. This is not hypothetical given that Stripe has already built many of the components it would require, they just exist as features rather than one unified product.

Stripe currently sits at the center of a small business’s financial life. When a customer makes a payment, Stripe collects funds and charges the appropriate taxes. During tax season, the platform helps streamline the filing process by holding accurate revenue records and sales tax data. From daily checkout to yearly compliance, Stripe already supports small businesses throughout key financial processes.

Currently, Global Payouts allows merchants to send money to any individual or institution worldwide. Consider what Stripe has build beneath the surface. Financial Connections enables businesses to read customers’ financial data through open banking APIs. Stripe Issuing helps companies launch their own commercial card programme, and Financial Accounts allows them to use Stripe as a digital banking platform.

Pulse would bring these touchpoints together into a single financial product. Instead of existing as separate features, Global Payouts would power bill pay, and Financial Connections would pull transaction records from external bank accounts into a unified view. Stripe Issuing would translate into spend controls, and Financial Accounts would continue to allow businesses to hold funds. Pulse is the layer that unifies what Stripe has already built.

With an average of 1,000 new companies joining the platform every day, Stripe can drive adoption of Pulse with near-zero acquisition cost. Through a freemium model, expense management and accounting deepens Stripe’s existing relationship with customers and opens up a new revenue stream.

To understand how this adoption happens naturally, consider a typical merchant’s path.

The Merchant Journey

A business looking to collect payments will most likely turn to Stripe. This is Stripe’s entry point into the ecosystem.

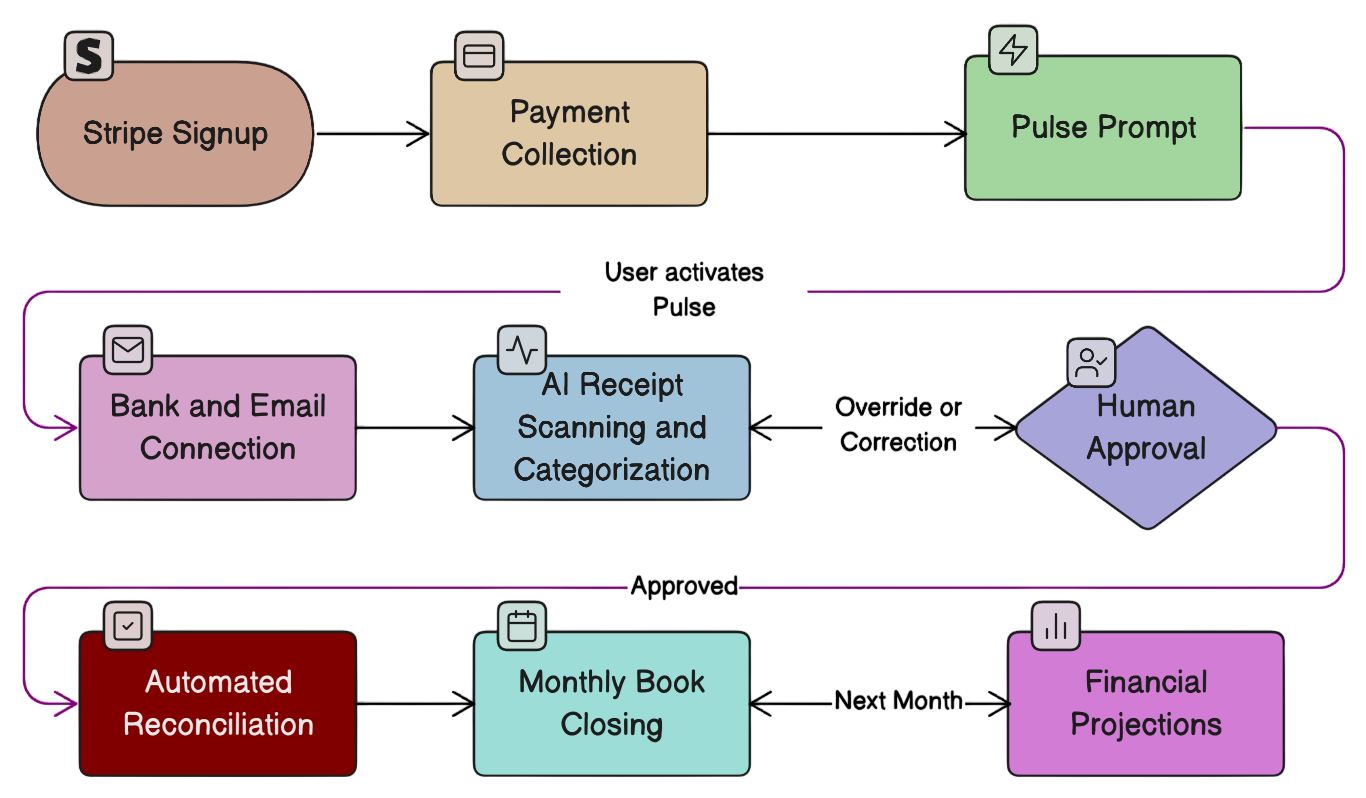

The business owner will quickly realize they lack a full financial picture. With a need to organize their transaction data, they will search for external software like QuickBooks. Before this even happens, Stripe can prompt them to activate Pulse instead.

Pulse then connects to the user’s Stripe Financial Account and any external bank accounts they choose to add. Transactions begin to flow through automatically.

From there, Stripe scans a designated email for invoices and receipts, using optical character recognition to extract data. Reconciliation processes, enhanced by generative AI, categorize transactions into existing expense categories or suggest new ones. Meanwhile, duplicate payments, missing receipts, and unusual spending patterns are flagged for action.

Following a human-in-the-loop model, the AI makes recommendations, but business owners retain final approval before anything is recorded or acted upon. This acts as a compliance measure, reduces errors, and builds trust with the user.

At the end of each month, Stripe walks the user through an assisted book-closing process. By analyzing a business’s typical revenue and spending patterns, Pulse will generate financial projections, giving business owners the clarity to budget more effectively. This includes revenue and expense forecasts, burn rate estimates, and recommendations for reducing spending.

By using Pulse, the ecosystem becomes stickier as it centralizes years of organized financial history and accounting data. Companies will become reliant on Stripe, eliminating any incentive to migrate their core payment processing elsewhere. However, building this kind of stickiness requires understanding why the tools that came before Pulse failed to do the same.

Figure 1: Stripe Pulse user journey from payment collection to automated financial operations.

Unmonitored: The Gap in the Market

Standing out in this market requires an understanding of where existing players fall short. Ramp and Brex appear to be the solution, but neither serves the type of business Stripe is targeting.

Brex dropped support for non-funded small businesses in 2022, instead choosing to focus on funded startups and enterprise clients. It now serves over 150 public companies. In January 2026, Capital One announced its acquisition of Brex for $5.15 billion, highlighting how far removed the company is from serving small businesses. Similarly, Ramp was initially framed as an expense management tool for startups, but now focuses on serving middle and upper-market companies, including Shopify, Figma, and Notion.

Neither product is designed for solo founders, five-person e-commerce teams, or small businesses without a dedicated finance team. Brex and Ramp have proven that financial tools for businesses are worth billions of dollars, yet companies are not building high-quality solutions for the smallest ones.

This creates an opportunity for Pulse to enter the market, as small businesses already log in to their Stripe dashboards daily to check sales volume. By prompting them to connect their external bank accounts for a unified financial dashboard, Stripe can leverage existing user behaviour and bypass the adoption curve of a standalone accounting tool. Pulse gives all founders a way to deeply understand their own numbers without the learning curve of traditional accounting software.

Understanding a business’s complete financial health unlocks potential across Stripe’s entire product suite. Stripe Billing could surface insights on profitability trends to inform pricing. Stripe Tax could generate smarter, pre-filled filings informed by categorizing expense data. Stripe Capital could offer more tailored loans based on real-time cash flow, accounts receivable, and burn rates. Each of these products becomes meaningfully better when powered by the holistic financial picture that Pulse provides. Pulse is a strong opportunity, but it is not without real challenges.

Irregular Rhythms: Where Pulse Could Go Wrong

By launching Pulse, Stripe enters the territory of its largest integration partners, including QuickBooks, Xero, and FreshBooks. These platforms may feel threatened and shift to building deeper integrations with Stripe’s competitors instead, like Paddle or Square. This risk could be mitigated by positioning Pulse as a tool for businesses that have not yet outgrown basic financial management.

For businesses that grow beyond what Pulse can offer, Stripe should work with enterprise resource planning (ERP) software that provides a more comprehensive accounting suite. A partnership would allow Stripe to have pre-built integrations with ERPs like SAP and Oracle, making the transition smoother and retaining larger customers who outgrow Pulse.

In a company as large as Stripe, small business tools could struggle for resources compared to high-margin enterprise products. If Pulse fails to show immediate scale, it risks feature stagnation, falling behind on changing tax laws or new bank API standards.

Pulse should not be viewed purely from the standpoint of growing direct revenue. Its value also lies in reducing merchant churn and increasing customer lifetime value across the entire platform.

With Stripe entering the accounting space, small business owners will inevitably ask Pulse tax and legal questions. Stripe, however, is a technology company, not an accounting firm. Providing automated financial tools creates a support liability where users expect Stripe to provide tax or legal advice, forming a massive regulatory and operational liability. Thus, Stripe should clearly recommend that users verify data with a Certified Public Accountant (CPA) and build a marketplace of Stripe-certified accountants who can provide professional guidance for a fee. Certified accountants will be composed of CPAs who hold a valid license and have completed a mandatory training curriculum from Stripe.

The Rollout: Where Pulse Beats First

Stripe should take a phased rollout approach, starting in the United States, where 99.9 percent of companies are small businesses. Doing so allows it to carefully manage regulatory complexities and monitor user feedback before scaling too quickly.

An invite-only beta should target a highly segmented cohort of Stripe users, limiting risk exposure while allowing the platform to be stress-tested. Progress should be measured through KPIs such as reconciliation error rate, user override rate, book-closing abandonment rate, and support ticket volume per user.

Once Pulse achieves product-market fit and internal benchmarks are satisfied, Stripe should launch its Certified Accountant marketplace to address the support liability. After the product is stabilized for the US market, Pulse can expand to the UK, Canada, and the EU, adapting to regional tax and compliance requirements.

To drive rapid adoption, Pulse could leverage a freemium model that automatically gives every Stripe user access to a unified cash flow dashboard. This free tier would benefit Stripe through increased platform stickiness and reduced churn. Advanced features, such as generative AI receipt matching, automated book-closing, and predictive cash-flow modelling, would be gated behind a monthly subscription or per-transaction model. This creates a new revenue stream that scales as the user’s business grows.

Building the Engine, Not Buying the Parts

As Stripe looks to bring Pulse to life, there are two paths it can take: building in-house or acquiring an existing company. Given Stripe’s development teams and existing infrastructure, building natively is the stronger choice. With many of the building blocks already in place, Stripe can design Pulse intentionally from the start, with deep integration into the existing product suite.

Acquiring an AI-native bookkeeping startup could accelerate the launch timeline, but it would leave Stripe with technical debt and the challenge of merging two user experiences into one. By building in-house, Stripe avoids these integration challenges and delivers a tool that feels like a natural extension of a business owner’s daily routine.

More Than a Payment Processor

Stripe’s overarching mission is to increase the GDP of the internet. One of the greatest barriers to that mission is the challenge of running a financially sound business online. By introducing Pulse, Stripe transitions from a payment infrastructure provider to an intelligent financial operating system for small businesses. It removes friction in back-office management and lets businesses focus on what matters most: building their products and serving their customers.

Editor(s): Isabella Pan, Affan Bhimani

Researcher(s): Miranda Lee, Brandon Feng