The Missing Link in Canada’s Nuclear Chain

By: Andrew Liu

The Ivey Business Review is a student publication conceived, designed and managed by Honors Business Administration students at the Ivey Business School.

A country that cannot feed itself, fuel itself, or defend itself has few options. — Mark Carney

At the World Economic Forum earlier this year, Mark Carney made striking remarks about the state of international affairs, claiming that Canada needed to prepare itself for the ‘new world order,' a statement that could not be more true in the world of energy. Over the past few years, reliance on international supply chains for energy has proven to be a detriment towards national security: the EU was unable to effectively sanction Russia after the invasion of Ukraine due to its dependence on Russian oil, natural gas, and uranium. The war in Iran has led to the closing of the Strait of Hormuz, resulting in increasing global liquefied natural gas (LNG) and oil prices, presenting a threat to energy security on a global scale. As a result, it is of utmost importance for Canada to seek out more reliable supply chains to meet their growing energy demands.

Despite longstanding opposition to nuclear energy following the nuclear meltdowns of Chernobyl and Fukushima, interest in nuclear energy has recently resurged as safety concerns have been mitigated and as countries seek to meet their growing energy demands, partially driven by the rise in AI data centres. Nuclear energy produces clean, consistent energy, with a smaller land footprint, making it a favorable option for countries balancing increasing energy demands and decarbonization. Currently, around 74 reactors are under construction globally and the US is aiming to quadruple its nuclear fleet by 2050.

Canada is uniquely positioned to meet this global demand due to its abundance of uranium ore. However, Canada lacks one crucial step in the nuclear fuel cycle, holding it back from being a one-stop shop for nuclear fuel and from developing a self-sufficient nuclear fuel cycle: enrichment facilities. In these times of political volatility, Canada should invest in enrichment facilities to access strategic independence and to continue being a nuclear energy leader on the global stage.

The Nuclear Fuel Cycle

There are five steps in the process to create nuclear fuel: mining/milling, refining, converting, enrichment, and fuel fabrication. First, companies mine uranium ore before milling it, or breaking it down into smaller particles, to allow for easier extraction of concentrated uranium called uranium oxide (U3O8). Uranium oxide is then refined to further purify the compound, transforming it into uranium trioxide (UO3), before being converted into uranium hexafluoride gas (UF6).

After conversion, reactors require enriched uranium to function. Uranium primarily comprises two isotopes, U-235, which comprises 0.7% of the ore, and U-238, which comprises the rest. U-235 is the isotope that undergoes fission, which is what generates nuclear energy.

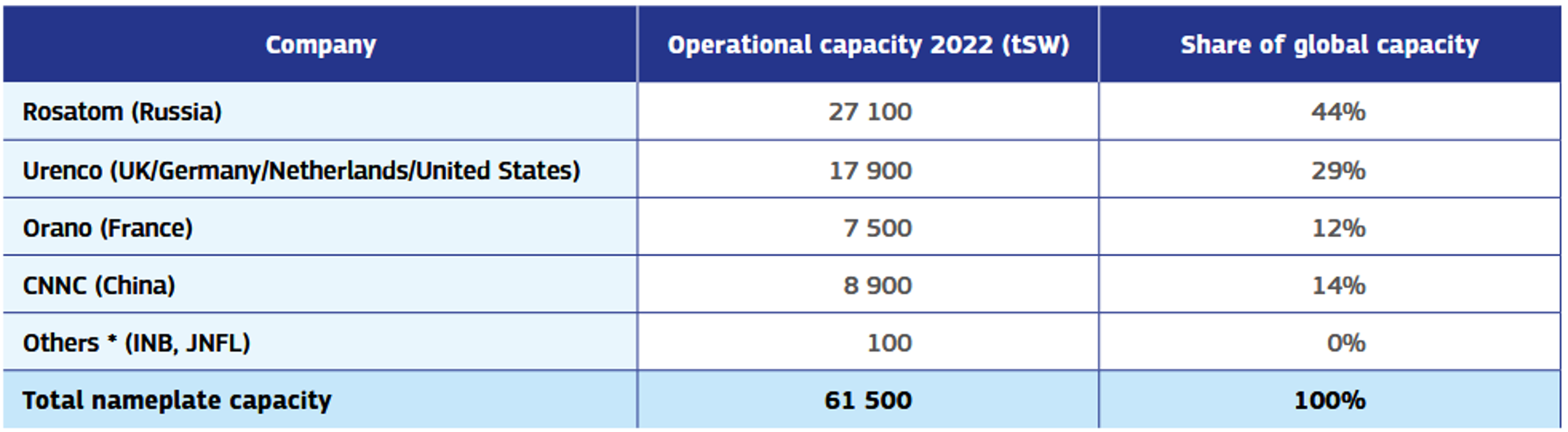

Nuclear fuel is typically grouped into two enrichment levels. Most existing light water reactors (LWR) use low-enriched uranium (LEU), which contains about 3.5–5% U-235. Newer and more advanced reactor designs often require higher concentrations of U-235, between 5–20%, known as High-Assay Low-Enriched Uranium (HALEU). After enrichment, the uranium is converted into uranium dioxide (UO2), which is formed into nuclear fuel. Currently, there are only four major companies that enrich uranium (Figure 1).

Figure 1. Global uranium enrichment supply. Source: Euratom Supply Agency, Annual Report 2024, reused under CC BY 4.0. Changes: None.

Canada’s involvement in the uranium fuel cycle: Why doesn’t it enrich its own uranium?

Canada is strongly integrated into the global uranium fuel cycle. It is the second largest producer of uranium (15% of global demand) and has the third largest uranium reserves in the world after Kazakhstan and Australia. Most of Canada’s uranium comes from Saskatchewan, which contains the largest high-grade uranium deposits in the world, with some being 100 times the world's average.

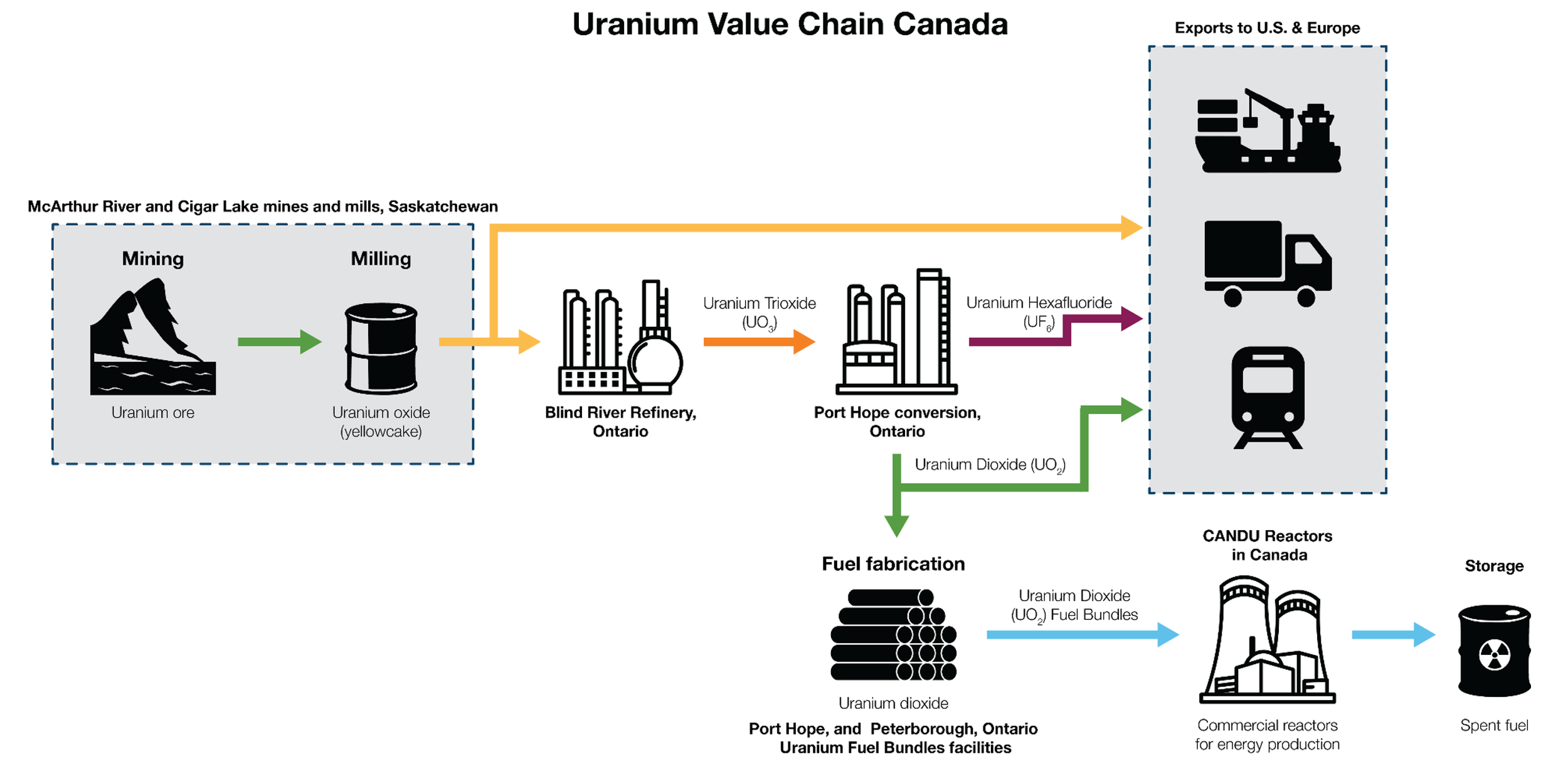

Canada also possesses significant midstream capabilities. Cameco, Canada’s largest uranium producer, operates the world’s largest commercial uranium refinery in Blind River and converts approximately 18% of the world’s uranium in Port Hope. However, Canada does not possess any uranium enrichment facilities.

Additionally, Canada is a leading innovator in nuclear reactor technologies. Canada Deuterium Uranium (CANDU) reactors have been sold to Argentina, China, India, Pakistan, Romania, and South Korea.

A key difference between CANDU reactors and LWR is that LWR requires enriched uranium, whereas CANDU reactors use natural/unenriched uranium. Because Canadian reactors have no need for domestic enrichment facilities, Canada instead utilizes natural uranium in its fuel or exports it to the US or Europe, where it is enriched for their domestic use (Figure 2). Therefore, it has historically not made strategic sense for Canada to develop uranium enrichment technology. However, Canada’s strategic paradigm is about to change.

Figure 2. Canadian Uranium Value Chain. Source: Canada Energy Regulator, “Market Snapshot: Canadian uranium exports help fuel nuclear generation around the world.” Figure taken from the version available on the CER website; this use has not been produced in affiliation with, or with the endorsement of, the Canada Energy Regulator.

The Future of Nuclear Energy: SMRs

Canada’s last domestic CANDU reactor was deployed in 1993, and its last international deployment occurred in Romania in 2007.[14] The reason why CANDU reactors are difficult to build internationally is that most countries are familiar with LWR technology. In fact, almost 90% of global nuclear reactors use LWR technology. Therefore, if Canada wants to be a stronger player in the nuclear power field, it must keep up with advancements in the industry and tailor its services accordingly.

Currently, many countries are developing small modular reactors (SMR). SMRs represent a new approach to reactor design and deployment, not a fundamentally different method of generating nuclear power. For instance, most SMRs currently use LWR technology to create nuclear energy. As suggested by its name, SMRs are smaller, modular, and safer in comparison to traditional reactors.

SMRs take up a 1/10th to 1/4th of the land footprint of a traditional LWR reactor, and they produce 300 megawatts electrical (MWe) compared to the 1000 MWe from traditional reactors. The modular nature of SMRs allows companies to reach economies of scale by manufacturing reactor parts before assembling them at a location, in contrast to traditional reactors which are custom designed for specific locations. SMRs are also safer because they rely on passive safety systems, such as natural circulation, gravity, and other physical forces, rather than the external electricity that traditional reactors require to shut down. The importance of this distinction was demonstrated at Fukushima, where the plant lost power after earthquakes destroyed the electrical grid, triggering the meltdown.

Another key benefit of SMRs is that they are able to generate higher heat levels for industrial uses. LWR-based SMRs can provide alternatives to natural gas and provide district heating and desalination plants. However, the “hardest-to-abate” industries — such as extraction of oil from oil sands, cement, and steel production — require high heat levels that only fossil fuels can currently produce. The next generation of SMRs after LWR-based SMRs are categorized as Generation IV SMRs, which use alternative coolants such as molten salt or gas rather than light water, and produce sufficiently high temperatures to decarbonize these industries. The only Gen IV reactor currently commercially operational is in China, which began operations in December 2023, and many others are in active development and are expected to reach deployment in the late 2030s to early 2040s.

Canada is a leader in SMR innovation, with its flagship Darlington New Nuclear Project (DNNP), an LWR-based SMR designated a project of national interest under Bill C-5 and backed by $2 billion CAD in federal investment, expected to open in 2030. However, Canada has no domestic enrichment capacity, forcing reliance on foreign suppliers; the government has already committed to backstopping up to $500 million CAD in LEU contracts from allied nations. This dependency, manageable for Darlington's near-term LEU needs, becomes a strategic liability as Canada moves toward Gen IV SMRs requiring HALEU.

One of the bottlenecks with developing Gen IV SMRs is the HALEU supply chain. Notably, the only two countries that produce HALEU are the US and Russia, with the latter being the only country that produces HALEU at a commercial scale. Recognizing the international reliance on Russian enrichment, many Western countries have started to invest in HALEU enrichment capacity. Recently, the US invested $1.8 billion USD in HALEU enrichment capacity and $900 million USD in LEU expansion, while the UK committed 156 million GBP to HALEU facilities. Despite these investments, Western enrichment capacity is unlikely to meet growing international HALEU demand, creating a significant opportunity for Canada to fill the gap and position itself as a leader in Gen IV SMR development.

Why is it an issue if Canada does not develop uranium enrichment?

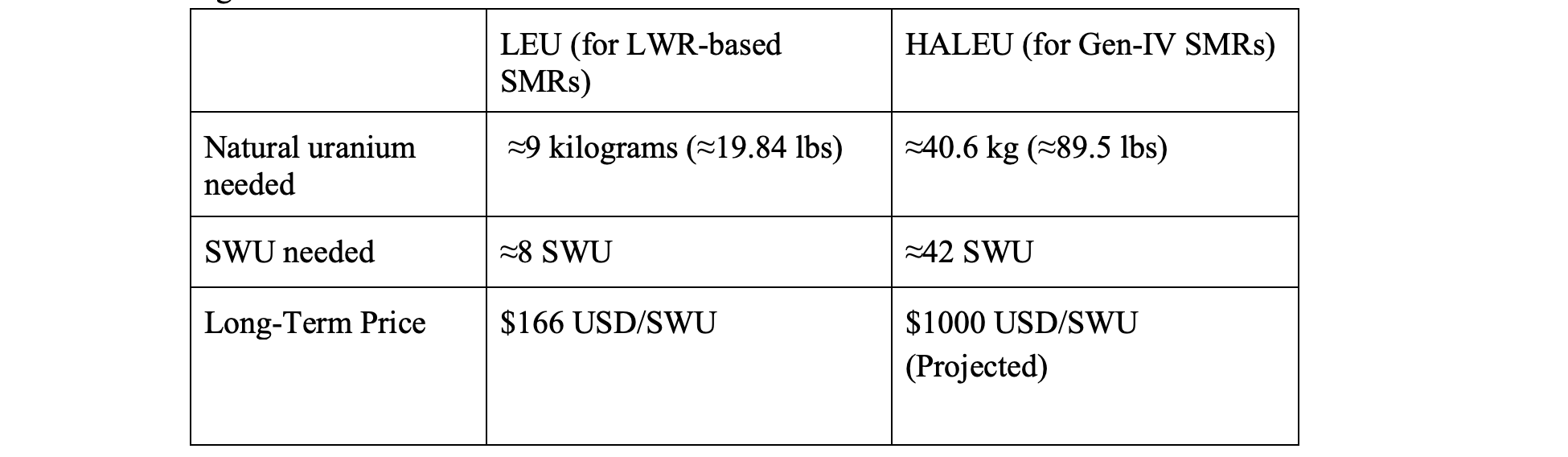

There are two issues if Canada does not build uranium enrichment facilities. First, the financial costs of building SMRs increase significantly if Canada were to import enriched uranium. Uranium enrichment is measured in separative work units (SWU), which measure how much effort is required to increase the concentration of the fissile isotope uranium-235 in uranium. In 2025, the average long-term price of uranium was $81.96 USD/lb. Without enrichment, Canada exports natural and converted uranium while other nations capture the enrichment premium, which represents nearly half the combined cost of uranium feed and enrichment services. Building domestic enrichment would allow Canada to retain this value rather than ceding it to competitors. The natural uranium and SWU required per kilogram of fuel vary based on target enrichment levels and the efficiency of the enrichment process (Figure 3).

Figure 3. Uranium and SWU needed to create 1 KG of LEU and HALEU

There are multiple factors that exacerbate the price. First, the market is dominated by an oligopoly, causing Canada to have little power over price. Second, price is further driven by geo-political conflicts. For instance, the Russian invasion of Ukraine in 2022 caused the price per SWU to increase from December 2021-December 2022 by 117%.

As a reference point, US companies paid approximately $1.5 billion USD for uranium enrichment services for its fleet of 94 LWR reactors in 2024, at an average contracted rate of $97.66 USD/SWU. If Canada were to build 85 reactors to meet its decarbonization goals, it would likely pay a substantial amount, as although they would require less enrichment services overall, they would face higher per-unit enrichment costs, as many of the US contracts were long-term contracts negotiated before enrichment prices surged following Russia's invasion of Ukraine in February 2022, meaning if Canada were to negotiate contracts today, it would need to pay the current long-term price of $166 USD/SWU, nearly 70% more per SWU than the US currently pays.

Furthermore, a full decarbonization plan with 85 SMRs would likely have many Gen IV reactors, which carry an estimated enrichment cost of approximately $1,000 USD/SWU, roughly 6x higher than the price of enriching to 1 kilogram of LEU. The total annual enrichment bill for Canada's proposed 85-SMR fleet would therefore represent a substantial and ongoing financial outflow to foreign enrichers.

In the US, estimates suggest a HALEU enrichment facility would cost approximately $4-5 billion USD to develop.[38] Even assuming higher costs in Canada due to the need to build new institutional knowledge, the investment case is still compelling: a single HALEU facility using centrifuge technology can simultaneously produce LEU, servicing Canada's entire 85-SMR fleet across both reactor types. At current market rates, the $1.5 billion USD Canada would pay annually to foreign enrichers suggests the capital cost could be recouped within 3-4 years, with additional upside from exporting enrichment services to allied nations facing similar supply constraints.

Second, Canada would lose strategic independence for its energy needs. Although Canada's allies are unlikely to restrict access to enrichment services, reliance on foreign capacity remains a strategic vulnerability. If such a worst-case scenario were to occur, Canada would be unable to shift its supply chains as enrichment facilities operate on long-term contracts. Notably, four years after the invasion of Ukraine, the EU still has not fully decoupled from Russian enrichment services despite significant investment in alternatives.

Additionally, if global SMR deployment accelerates, Western enrichment capacity may be insufficient to meet both domestic and allied demand simultaneously. This would further increase the already significant enrichment costs outlined above and compromise Canada’s ability to meet its decarbonization goals.

International Opportunities for Uranium Enrichment

The EU’s reliance on Russian uranium

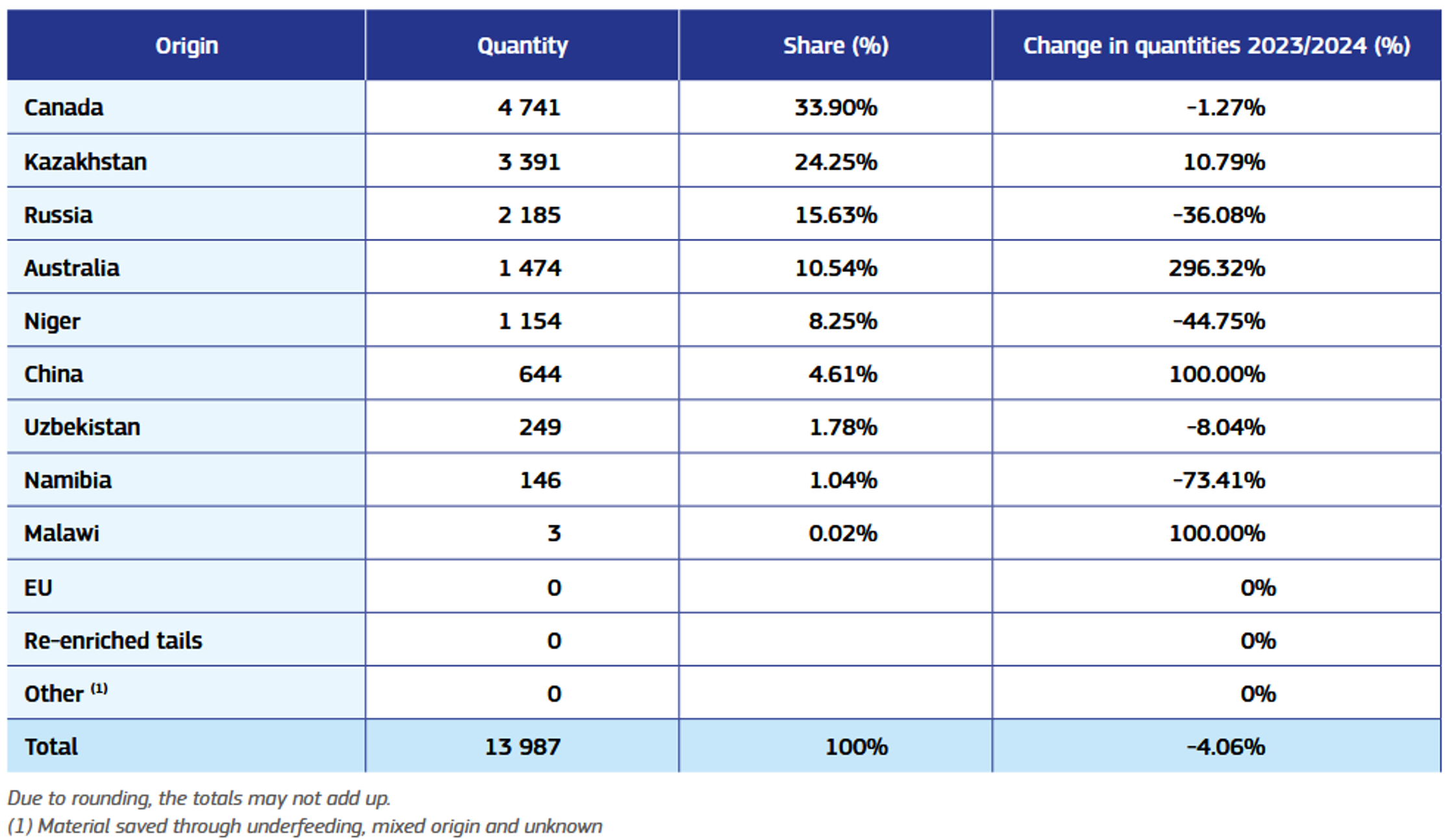

Although the EU has sanctioned many Russian companies and has shifted its supply chains in natural gas, oil, etc., one company it hasn’t yet sanctioned is the Russian state-owned Rosatom. To combat this, the EU has tried to reduce reliance on Rosatom by shifting much of its raw uranium supply away from Russia to nations such as Canada and Kazakhstan (Figure 4).

Figure 4. Origins of EU uranium supply. Source: Euratom Supply Agency, Annual Report 2024, reused under CC BY 4.0. Changes: None.

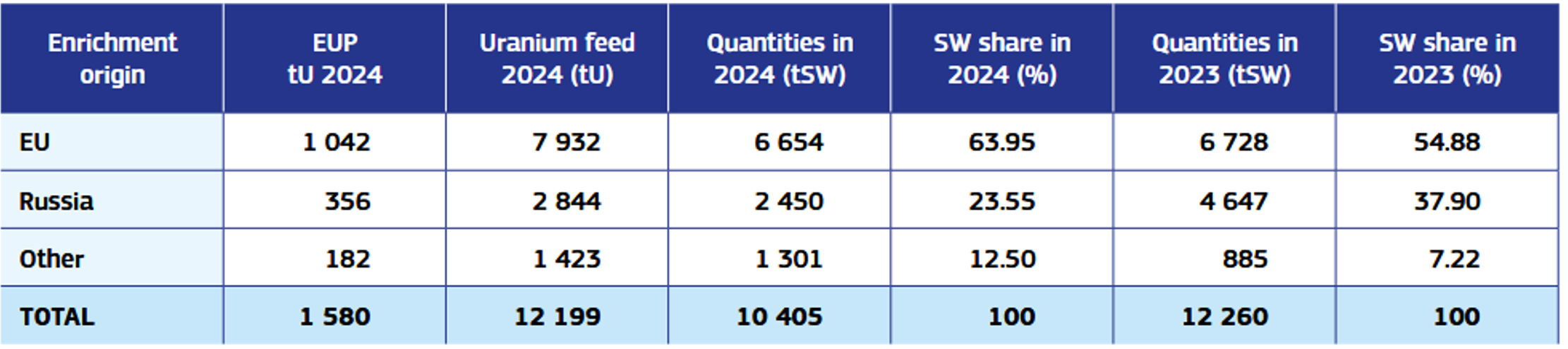

However, the EU remains reliant on Rosatom for uranium enrichment services (Figure 5). Currently, the EIB has invested 400 million EUR to expand Orano’s Georges Besse 2 enrichment plant, but it is not enough to make the EU self-sufficient from Russian enrichment services. While the EU also faces challenges in replacing Russian fuel fabrication for Soviet-era reactors in Eastern Europe, the most significant opportunity for Canada lies in enrichment services. Canadian enrichment capacity would provide the EU with an additional Western supplier, further reducing its dependence on Rosatom.

Figure 5. Origins of EU enrichment services. Source: Euratom Supply Agency, Annual Report 2024, reused under CC BY 4.0. Changes: None.

Meeting the growing energy demands of developing countries: ASEAN

Another opportunity for Canada to increase its market share is by becoming a one-stop shop for countries interested in nuclear energy. An area where Rosatom has historically outcompeted other alternatives to nuclear energy has been its ability to provide a complete package for countries. Since Rosatom possesses uranium mines, refineries, and technology to build nuclear plants, it acts as a one-stop shop for companies seeking contracts. However, continued sanctions have harmed Rosatom’s ability to become an international partner, allowing Canada to potentially replace Rosatom as a politically viable one-stop shop if it can expand its current capabilities to include enrichment.

The Association of Southeast Asian Nations (ASEAN), is one of the fastest-growing economic blocs in the world (Figure 6). It possesses developed economies in Singapore, as well as rapidly growing economies in Vietnam, Malaysia, Indonesia and Thailand. ASEAN needs to find a way to balance growing energy demands caused by its rapid economic growth, AI development, and increased digitization, with its growing pressures to decarbonize to combat climate change. Countries such as Myanmar, the Philippines, Thailand, and Vietnam are among the most affected nations in the world by climate change. As a result, several ASEAN countries have been looking to invest in SMR technology rather than traditional reactors.

Figure 6. ASEAN Nations. Source: RizkyJogja, “Map and flag of ASEAN countries,” Wikimedia Commons, CC BY-SA 4.0. Changes: None.

Although Canada has been promoting its nuclear expertise across ASEAN through the Canadian-ASEAN Business Council (CABC), Canada’s lack of enrichment services would harm Canada’s ability to position itself as a partner.[45] ASEAN could source natural uranium from Kazakhstan, utilize American/European uranium enrichment services, and implement Chinese SMR technologies. As a competitive advantage, Canada could pitch itself as a one-stop shop for nuclear energy. With domestic enrichment, Canada could offer a simpler, more integrated alternative: a complete nuclear fuel supply chain from a single trusted Western partner, reducing the complexity and geopolitical risk of multi-supplier arrangements.

The geopolitical stakes of ASEAN's nuclear development extend beyond commercial opportunity. China and Russia have long used energy as a means of building long-term strategic dependencies. Relationships that start off as economic ones inevitably turn into political reliances as countries become reliant on China or Russia to power themselves. Canada's entry as a Western nuclear partner would offer ASEAN nations an alternative that does not carry the same geopolitical baggage, keeping critical energy infrastructure within the Western sphere of influence. For Canada, energy trade could serve as a catalyst to diversify its strategic partnerships beyond its heavy reliance on the United States and China, building durable economic ties with one of the world's fastest-growing regions.

How should Canada develop uranium enrichment?

As uranium enrichment is an issue of national security, it is an endeavour that companies must partner with governments to pursue. The biggest barrier to Canadian companies currently is that Canada does not have a uranium enrichment regulatory framework. To create a new set of regulatory frameworks, Canada could utilize the International Atomic Energy Agency’s (IAEA) safeguard frameworks, borrow from American/European enrichment regulations to expand upon its existing uranium regulatory framework for mining and conversion. As Canada is a part of the Treaty on the Non-Proliferation of Nuclear Weapons, it would likely need to work with the IAEA to have consistent monitoring, ensuring that Canada does not develop nuclear weapons.

The fastest way for Canada to develop uranium enrichment technology would be to leverage its international partnerships. The world’s first Western commercial centrifuge-based uranium enrichment facility was built by Urenco after the Treaty of Almelo was signed in 1970, a trilateral agreement signed between the UK, Germany, and The Netherlands. The three countries agreed that any new country wanting to receive uranium enrichment technology would need to abide by Non-Proliferation agreements, and consent from all three countries. Since then, the US received uranium enrichment technology when they signed the Treaty of Washington in 1992 and when France signed the Treaty of Cardiff in 2005. Canada should pursue a similar Treaty of Ottawa with the UK, Germany, and The Netherlands to access uranium enrichment facilities.

Under this model, as demonstrated by the US experience, Urenco would operate an enrichment facility on Canadian soil using their proprietary technology, giving Canada domestic enrichment capacity without requiring independent development of centrifuge technology from scratch. Over time, a Canadian company could pursue a deeper ownership stake in the facility. This would mirror France's approach, where Orano acquired a 50% stake in Enrichment Technology Company (ETC), the joint venture through which Urenco's centrifuge technology is owned and licensed, following the signing of the Treaty of Cardiff in 2005.

The value that Canada would provide to the UK, Germany, and The Netherlands is significant: Canada would be able to alleviate the reliance of the EU on Russian uranium enrichment services, and allow further global developments of HALEU technology, at a crucial time where there is a race between the West, Russia, and China to deploy Gen IV reactors. For the Almelo signatories, Canada's clean nonproliferation record, its existing IAEA safeguards obligations dating to the earliest days of the agency, and Cameco's established role as an indispensable upstream partner in Western nuclear fuel supply chains collectively demonstrate that Canada can be trusted to abide by international non-proliferation treaties.

The second pathway is through SILEX laser enrichment technology. Global Laser Enrichment (GLE) is a US-based company and the exclusive licensee of SILEX laser enrichment technology, jointly owned by Cameco (49%) and Silex Systems Limited, an Australian company (51%). Cameco holds an option to acquire up to 75% of GLE, subject to US government approval. SILEX is a new-generation enrichment technique targeting commercial deployment by 2030. However, Australia and the US maintain a bilateral agreement restricting the sharing of SILEX intellectual property. Canada would need to negotiate entry into this agreement, a significant diplomatic undertaking. However, the foundation for such an agreement already exists: the Canada-US 123 Agreement provides a framework for nuclear cooperation and fuel cycle development, and Cameco's ownership stake in GLE gives Canada a direct commercial interest in the technology.

Out of the two pathways, the Urenco pathway offers proven, commercially deployed technology with clear treaty precedent for expansion, making it the more viable near-term option. The SILEX pathway leverages Cameco's existing ownership position and could provide a technological edge, but depends on a technology that has not yet been commercially proven and requires US and Australian approval.

If international negotiations prove unsuccessful, Canada is not without alternatives. It could pursue domestic development of enrichment technology, a longer and more costly path, but one that Canada's nuclear engineering expertise and research infrastructure could support. In the interim, Canada could secure long-term enrichment contracts with allied suppliers or co-invest in expanding existing Western enrichment facilities in exchange for guaranteed supply. Regardless of the pathway, the first step remains the same: establishing a domestic regulatory framework for enrichment and signaling clear political intent.

Regardless of what pathway Canada chooses, a public-private partnership between the Canadian government and Cameco would be vital. Cameco's role in the nuclear fuel cycle makes it a natural choice for a domestic enrichment program. On the government side, the Strategic Response Fund (SRF), which recently received $5 billion CAD, is designed to support strategically important industrial investments, while the Major Projects Office (MPO) would streamline the regulatory approvals that a first-of-a-kind Canadian enrichment facility would require.

Conclusion

Canada possesses nearly every element needed to be a global nuclear leader: world-class uranium deposits, the largest commercial refinery, significant conversion capacity, and a history of reactor innovation. The missing piece is enrichment. Without it, Canada faces approximately $1.5 billion USD in annual enrichment costs to fuel its SMR fleet, cedes the most valuable step in the nuclear fuel cycle to foreign competitors, and leaves its energy security and decarbonization targets vulnerable to geopolitical disruption.

The opportunities are clear: the EU needs Western alternatives to Russian enrichment, ASEAN nations are seeking trusted nuclear partners, and global demand for HALEU is outpacing supply. The pathways exist, whether through a Treaty of Ottawa with the founding Urenco nations or through SILEX laser technology. What Canada needs now is the political will to act. In a world where energy sovereignty is national security, Canada cannot afford to leave enrichment to others.

Editor(s): Ken Sue-A-Quan & Ava Testa

Researcher(s): Chaitrali Patil