TD: Floating an Opportunity

By: Shaw Kim

The Ivey Business Review is a student publication conceived, designed and managed by Honors Business Administration students at the Ivey Business School.

TD: Floating an Opportunity

Float Financial was founded in 2020 by Ruslan Nikolaev and Griffin Keglevich, with Rob Khazzam appointed as CEO in 2021. Founded in Toronto, Canada, the fintech provider started with a corporate card and expense solution, which has since grown to include AP automation and working capital credit solutions, now used by over 6,000 Canadian small and medium sized businesses (SMEs). No longer did SMEs need banks to receive this financial operating system.

TD has a client base of a million small businesses, which translates to a high disruption exposure. This means that the decisions that will be made in the near future may come to determine the future strength of TD's SME book as fintech disruption is on the rise.

Cracks in the Foundation

Canada’s SME banking market is large and restless, with SMEs employing 63.6 percent of the private sector workforce, and Canada's retail and SME banking market size stands at $135 billion as of 2022. Despite the obvious need for innovation in the Canadian financial market, Canada's fintech penetration stands at 3% as opposed to the 8% penetration in the US, creating a $5 billion dollar gap in the Canadian banking market.

The challenge of financing access was apparent in a survey which found new loans to small businesses fell 19 percent while large business lending grew 14.4 percent over the same period. Canadian SMEs pay roughly double the OECD average premium over large-company borrowing rates (the spread between SMEs and large businesses in Canada was 1.64 and 2.10 percentage points in 2021 and 2022 compared to an OECD average of 0.93 and 0.90 percentage points over the same years). Meanwhile, 66 percent of small businesses were required to pledge collateral to access credit in 2024, up sharply from 46 percent the prior year.

Satisfaction is deteriorating in parallel. Overall small business banking satisfaction fell 21 points year-over-year to 655 out of 1,000 in 2024, with TD tied for third among the Big Five at 656. While only one in ten business owners made the switch between 2019 and 2022, one in five wanted to.

Float Financial: More Than Meets the Card

While Float may look like a corporate card company on the surface, the real product is the financial data engine underneath. The card itself isn’t the whole story, it's part of a much more compelling product offering. Float wraps it in real-time spend controls and per-employee limits across CAD and USD, then stacks expense management with automatic receipt scanning. Float also automates bill payments. Its headline offering is up to $3 million in interest-free credit, approved based on how cash actually flows through a business rather than past financial statements. In September 2025, Float launched business accounts that allow for holding USD and CAD, currency conversion, and earning up to 4 percent interest, thus completing the operating loop with QuickBooks and Xero.

Every transaction Float process deepens its underwriting model, something TD cannot replicate through its existing underwriting model. Float’s credit engine runs against live transactional data, whereas a bank’s credit committee works with lagging historical financials. For fast-growing small businesses, the ones banks struggle most to serve, that gap widens with each client Float adds. As of January 2025, Float reached $30 million in annual revenues across 4,000 customers, with revenues having grown 50x and total payment volume by 45x since its Series A. A fintech sustaining those growth rates while extending same-day credit without personal guarantees is not doing so on wishful underwriting.

Float’s raise trajectory confirms institutional conviction. The company closed a CAD $70 million Series B led by Goldman Sachs Alternatives in January 2025, alongside OMERS Ventures and others. Twelve months later, in January 2026, Float secured a nearly $100 million CAD debt facility, enough to back $1.5 billion in annual client spending, a significant expansion in how much credit it can extend.

TD’s Gap No Partnership Can Close

TD enters 2026 with a focused domestic mandate. After a regulatory penalty in the U.S. over anti-money-laundering failures, CEO Raymond Chun has refocused TD on growing its Canadian business. The cap on TD's U.S. operations, imposed as part of that penalty, does not restrict what TD can buy in Canada.

TD's Canadian retail and commercial bank earned $1.87 billion last quarter while business lending grew 6 percent year over year. That franchise is the opportunity. It is also the exposure. TD’s existing fintech partnerships do not address it. The FISPAN partnership, launched in 2022, connects banking data to corporate accounting systems for U.S. commercial clients. After four years, TD is still rolling out basic payment initiation. FISPAN does not serve Canadian SMEs, and it does not touch corporate cards, expense management, or working capital credit. The July 2025 partnership with Fiserv and Clover helps businesses collect payments from customers. Float does the opposite: it helps businesses make payments and manage spending. As of 2026 TD has no Canadian product for real-time spending controls or credit based on live cash flow. It also lacks automated bill payment or high-interest business accounts. Building all of this from scratch would take years, cost hundreds of millions, and still leave TD without the lending data Float has already accumulated.

Two Deadlines That Cannot Be Negotiated

There are two key regulatory events which will forever change the value of Float and the leverage of TD. The same factors which limit the acquisition window for TD also expand the upside for Float independently.

OSFI, Canada's banking regulator, plans to fast-track banking license applications in 2026. A prepared applicant could go from filing to operating in as little as eighteen months. This framework is also designed specifically for large-scale digital lenders, fintech's and neo-banks. Float’s profile matches this exactly.

With the framework in mind, it’s important to note that the “de facto” deadline is not when Float gets its banking license but rather when Float files the application and the market finds out. That filing signals intent, triggers competitive re-pricing, and eliminates TD’s current pricing advantage. The window compresses when the market re-prices Float as a bank-in-progress, not when it formally becomes one.

The Consumer-Driven Banking Act (a part of Bill C-15), if passed, would force banks to share customer data through standardized connections by mid-2027. That means a customer could move their banking relationship to Float in seconds, not weeks. The law would replace today's clunky workarounds for sharing financial data with a secure, standardized system. If moving a banking relationship takes thirty seconds instead of thirty days, the factor that causes customer stickiness at TD disappears. A strong case study of this is the UK, where there are 13.3 million active open banking users as of March 2025 which caused a significant reduction in switching costs as competitors improved their offerings around the operating system. The takeaway from the UK for TD is that acquiring Float before mid-2027 means TD owns the interface SMEs use daily. A partnership after mid-2027 means TD is a credit utility clients access quarterly through Float’s network, and one Float can walk away from without losing a single client relationship.

Partnership or Acquisition?

The immediate reaction to this reasoning is a commercial partnership, where they split the revenue of Float’s product through TD’s distribution network without the need for costly and troublesome integration. Open banking does not just make a partnership insufficient. It makes one dangerous.

In a world previous to the Consumer-Driven Banking Act (CDBA) taking effect, Float needs TD’s distribution network to reach SME clients in bulk. Once the act is brought into effect, Float will have access to TD’s client data through a simple client click for consent. A commercial partnership, agreed upon today, will only serve to accelerate client acquisition for Float through TD’s distribution network, and will have no utility for Float once write access is live.

The strongest counterargument is that TD could structure a partnership with contractual protections: the right to buy Float later, limits on Float partnering with competitors, or an automatic trigger if Float applies for a banking license. These clauses are feasible on paper but would never be accepted by Float's investors who seek commercial upside. Float's investors did not put in millions to have their upside limited by a contract with TD, especially when regulatory tailwinds are about to make Float more valuable.

A right of first refusal protects TD from losing Float to a rival, but it does not stop Float from getting a banking license or going public in the U.S., both of which would make Float far more expensive to buy later. A more traditional option is a minority equity investment in a future financing round, coming in as a strategic investor without acquisition rights. This would satisfy Float's investors, but it does not give TD what it actually needs. A passive investment in Float gives TD no control over Float's technology, no access to its lending data, and no ability to block a rival from buying Float outright. All it does is confirm Float's value to the rest of the market.

Three more compounding issues are present behind this structural point. A partnership gives TD access to Float's interface, not its brain. The lending intelligence Float has built from millions of transactions stays with Float since a business agreement does not stop competition. Capital One's $5.15 billion acquisition of Brex in January 2026, the largest bank-fintech deal in history, shows that major players are buying spend management platforms outright. Another key argument against a partnership is the complexity of such an arrangement with over two-thirds of fintech insiders surveyed by McKinsey saying bank partnerships were plagued by slow deal timelines of up to two years, expensive compliance demands, and restrictive exclusivity clauses.

Why Float Would Sell

The most intuitive counterargument is self-evident: when Float is expanding at a rate of around 50 to 80 percent per annum over its major metrics, possesses a Goldman Sachs-led Series B, has just unlocked a billion and a half annualized spending potential, and is itself operating in a regulatory environment that is on the verge of structural expansion of its addressable market, why would it sell at all?

Growing by accessing public markets is also not as easy as the momentum of Float would imply because going public on the TSX is not a realistic path. The exchange produced only 19 IPOs worth $1.54 billion in all of 2025. A U.S. listing is more realistic, but it creates a contradiction: Float's competitive advantage is built entirely on being Canadian, which makes it a harder sell to American investors. Public markets in 2026 are rewarding companies that already make money, not those still spending to grow. Float's own January 2026 report showed that Canadian business revenues grew only 5 percent in 2025, and rising costs squeezed profit margins, directly putting a strain on the expansion runway of Float.

Float's investors need to cash out eventually. In 2025, with an exit value of 104.4 billion on 486 exits, global fintech VCs had the third-largest annual exit on record. OMERS Ventures, Goldman Sachs Growth Equity, FJ Labs and Teralys are not non-definite holders. Goldman Sachs-style investors typically want a return within four to seven years. A buyout from TD at the right price is more likely to deliver that return than a shaky IPO which ups the incentive for Float’s board of investors.

Getting a banking license is not free. It comes with heavy capital and compliance costs that Float may not want to take on. A Canadian banking license requires holding a large cushion of backup capital, roughly 10.5 percent of risk-adjusted assets, plus meeting additional safety requirements., which would divert capital that Float could use to invest in product development and customer acquisition. Every dollar locked up in regulatory reserves is a dollar Float cannot spend on lending or building new features which has been the force behind the development of Float thus far. The sale to TD will enable the investors in Float to crystallize the returns without Float ever incurring those expenses, and the current capital infrastructure of TD bears the regulatory burden without being seen.

Timing may matter most. Float has grown largely without a serious competitive response from the big banks, but there are signs that is changing. RBC's purchase of HSBC Canada's commercial banking clients in 2024 showed it is willing to spend aggressively on growth. TD’s Big five competitors have also accelerated fintech investments. Once a big bank builds or buys a competing product, winning new SME clients becomes far more expensive for Float, and its negotiating leverage in an acquisition weakens. The best exit point is now, when Float has momentum, and its competitors have not yet mobilized full force, since the latter can leverage this gap. The four- to seven-year implied hold horizon of the Goldman Sachs-led Series B means that the acquisition window is probably in the middle of its term.

The Mystery Bank

Float’s January 2026 debt facility includes an undisclosed Canadian Schedule I bank alongside Silicon Valley Bank, collectively providing nearly CAD $100 million. The anonymity creates a complication TD must treat as a priority due diligence item.

Whichever institution holds Float’s debt facility has already conducted credit due diligence on Float’s receivables, assessed its underwriting model, and established a commercial relationship from the inside. That inside knowledge is a head start. And debt contracts of this size typically include clauses that let the lender demand repayment or block a sale if the company changes hands. If TD is not the mystery lender, it could be trying to buy a company where a rival bank has the contractual right to block the deal. On the flip side, if TD is the unnamed lender, the calculation works in the opposite direction, since TD already has material due diligence on the credit book of Float, and should be capable of acting quicker than any competing bidder.

Float has not publicly named the bank, which is unusual for a financing announcement designed to signal credibility. The most likely reason is that the bank did not want to telegraph strategic interest, which suggests the relationship runs deeper than a standard lending arrangement. Identification of this lender should be a precondition of any term sheet made by TD, determine whether the debt contract gives that lender any power to block or delay a sale, and if so, structure the deal to pay off or absorb the debt at closing.

What TD Is Actually Buying

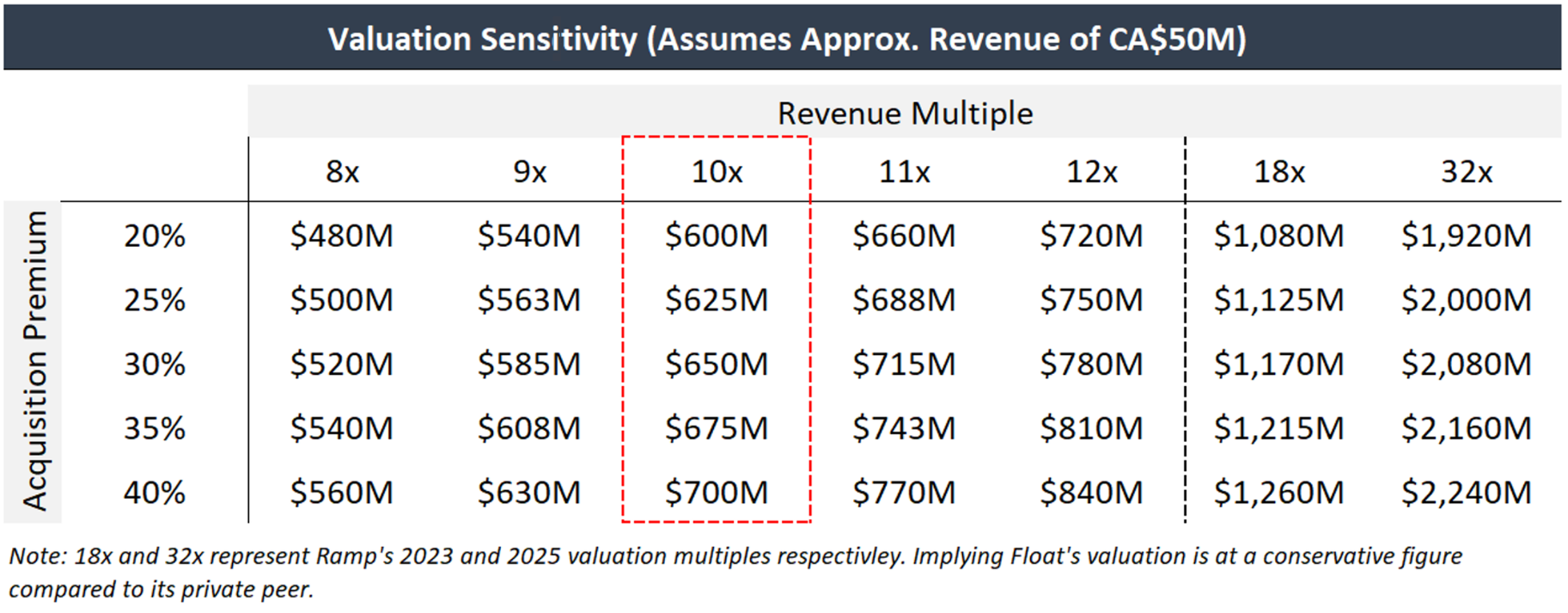

Float reported approximately $30 million in annual revenues across 4,000 customers in January 2025. With 6,000 customers as of January 2026, a 50 percent increase, a current ARR (annual recurring revenue) in the CAD $45 to $55 million range is a defensible estimate, assuming revenue per customer has remained broadly stable. The caveat to that assumption is that when Float launched business accounts with 4 percent interest in September 2025, it may change the income mix per customer, but the trend is unclear, increased product adoption would offset dilution by customers brought onboard at a lower initial monetization. When the acquisition range is north of 10x revenue, the acquisition would likely be at a valuation above CAD $500M, aligning with precedent transactions and ensuring Series B investors are able to receive an acceptable return.

The category has a precedent of multiple. The closest U.S. comparison is Ramp, which was valued at $5.5 billion on $300 million in revenue in 2023, roughly 18 times annual revenue, even after a significant market downturn. Ramp's November 2025 round valued it at $32 billion on $1 billion in revenue, signaling that investors are willing to pay much higher prices for fintech platforms that offer a full suite of products. Float is yet to enjoy the same re-rating: it is in a smaller addressable market, is not yet profitable and does not have the product breadth that propelled Ramp to numerous expansions. The 10 to 15x assumption made by Float factors in those discounts in. The transaction between Capital One and Brex of 5.15 billion is another confirmation of the upper limit of this scale of spend-management platforms. This is also in line with the larger Canadian fintech acquisition context: smaller VC-backed Canadian fintech acquisitions in 2024 had an average deal value of 19.5 million, which is indicative of a market rewarding scale disproportionately, and the Nuvei take-private at 6.3 billion was a payments processor acquisition, and is not a structural analog.

TD can absorb a transaction of this size without straining its capital position as the bank holds significantly more backup capital than regulators require, roughly three percentage points above the minimum. The complication is that Float's loans to small businesses, most of which have no collateral, are treated as riskier under banking rules than TD's mortgage-heavy portfolio. That means every dollar of Float's lending requires TD to hold more capital in reserve. In practice, the big banks hold capital above the regulatory minimum as a buffer, so TD's true spare capacity is closer to 1.5 to 2 percentage points. But higher risk weights per dollar of Float’s lending also mean higher revenue per dollar of capital deployed. TD’s existing P&C book is dominated by thin-spread mortgages. Return on risk-weighted assets, not absolute RWA, is what shareholders price. There is a longer-term benefit too: if Float's lending data shows lower losses than the models initially assume, TD can eventually reduce the capital it holds against those loans, freeing up even more capacity.

TD launched TD AI Prism in mid-2025, a predictive foundation model built by Layer 6 designed to anticipate customer needs across dozens of product categories simultaneously. TD AI Prism is currently trained primarily on retail and personal banking data. Float’s real-time SME transactional data, covering corporate card spend patterns, accounts payable flows, supplier payment cycles, and cash conversion behaviour, represents a data category TD has no meaningful access to at this depth. Acquiring Float feeds this data into TD AI Prism, extending its predictive capability into the SME segment. Better SME data produces better credit models, which let TD approve the high-growth businesses it currently declines. Those approvals generate more transactional data, and the loop tightens from there. Layer 6 grew from roughly 20 colleagues at acquisition in 2018 to over 200 today. No partnership replicates this.

Float currently pays for its high-interest business accounts by borrowing from outside lenders. If TD owns Float, it can fund those accounts with its own deposits, which are far cheaper, and keep the difference. Float's 6,000 clients each keep cash in their accounts. Under TD's ownership, those balances become cheap funding for the bank instead of an expense Float pays to outside lenders.

The model by Float is also aimed at SMEs which are generally neglected or rejected by the normal bank lending procedures and helps to open credit facilities to those businesses. It is a two-sided win: TD gets more lending volume and lower risk, because Float monitors how businesses spend and pay in real time, catching trouble signs months before a traditional quarterly review would. At the midpoint, TD is paying less than 4 percent of its Canadian P&C revenue. For the operating layer of the country’s SME economy, that is cheap.

The Subsidiary Question

The acquisition structure matters as much as the price. Float should operate as a wholly-owned subsidiary with its brand intact, following the same model TD used for Layer 6. TD acquired Layer 6 in January 2018 for over $100 million and kept it as a named internal centre of excellence with its own identity, growing the team from roughly 20 to over 200 AI specialists while fully integrating its work into TD’s products. The outcome was sustained talent retention and faster product delivery without losing the technical culture that justified the price. The playbook applies directly.

Float’s brand credibility with SMEs is part of what TD is acquiring. Six thousand businesses chose Float precisely because it does not feel like a bank. Absorbing Float into TD Business Banking and retiring the brand would risk eroding the client stickiness the acquisition is premised on. Float’s switching cost is functional, baked into accounting integrations and embedded workflows. But it is also attitudinal: SMEs chose Float because it does not feel like a bank. That perception does not survive rebranding. Float should operate as TD’s SME fintech subsidiary: its own product roadmap, its own founder leadership, TD’s balance sheet behind it. Integration happens at the data layer and the credit facility. The product interface stays Float’s.

The Clock Is Already Running

The deadline for the OSFI filing and the previously unnamed tier-one bank already embedded in the debt structure of Float may have predetermined the choice of TD in its favor. TD is the natural acquirer by virtue of its domestic mandate, balance sheet capacity, and 1 million SME clients. The OSFI fast-track, and the upcoming Consumer-Driven Banking Act, narrow the window down into particular months. This is not a fintech experiment, at CAD $600 to $700 million. The OSFI calendar is an administrative fact. The CDBA plan relies on the passage of legislation that is not yet certain. It does not matter which deadline arrives first. If TD has not acted by the time either one hits, the result is the same: Float becomes harder to buy and more expensive to lose.

Editor(s): Shalin Ratti, Juvhan Nithi & Kassem Kanjo

Researcher(s): Justin Chen