Serie A: The Fall and Inevitable Rise of a Giant

By: Stefan D’Amato

The Ivey Business Review is a student publication conceived, designed and managed by Honors Business Administration students at the Ivey Business School.

Rise, Fall, and Stagnation: How Serie A Lost Its Edge

In the period of the 1980s and 1990s, Serie A reigned as the highest quality showcase of football talent and financial structure. Between 1989 and 1998, Italian teams reached the final 9 out of 10 times, winning four of those finals, showing consistent high quality performances and attraction of talent. The 2000s however, brought upon a large change of corruption, financial mismanagement, and lack of oversight from governing bodies. By the early 2000s, S.S. Lazio’s owners defaulted on long term low interest loans, along with Parma, Napoli, and Fiorentina. Such episodes underscored that much of the wealth available in the 90s was built upon fragile corporate empires and reckless spending overall. Modernization efforts were also harmed by previous actions, as most clubs played in stadiums they did not own, and modernization of infrastructure was incredibly slow paced, not matching the rest of European leagues.

European football is unlike typical North American sporting structures. For one, there are multiple leagues which serve as domestic competition between clubs, as well as a stepping stone to UEFA competitions. The five largest European football leagues in the world are separated by country/region. The Premier League in the United Kingdom, Serie A in Italy, Bundesliga in Germany, La Liga in Spain, and Ligue 1 in France. These leagues are not only the largest in the European landscape, but also the largest in the world in terms of footballing quality, club size, and revenue. For large clubs within the system, it is expected for them to qualify for UEFA competitions every season. This is done usually by finishing in the top 7 places out of approximately 20 teams (Bundesliga has 18 teams, with the top 6 qualifying for Europe). The fifth to seventh place teams usually compete in either the UEFA Europa League, the second biggest European competition, or the UEFA Conference League, which only originated in 2021 and is the lowest tier of the European Tournament structure. The illustrious “Top 4” is usually what teams chase in conjunction with their respective domestic title. Finishing in the Top 4 secures qualification to the UEFA Champions League, the most prestigious tournament in club football. Teams that qualify for European football do not only benefit from the prestige and additional ticket sales, but from prize money allocated at UEFA’s (the governing body of football in Europe) discretion. This past year, the Champions League prize pool was that of €2.4 billion ($2.9 billion). Along with the guaranteed prize pool, there are a number of incentives for performance throughout all three competitions (Exhibit 1). These ranges are heavily dependent on performance in the initial league phase and throughout the competition. The main point however, is one; the glaring disparity between competitions, and two; the amount of additional revenue that teams have the chance to earn.

The New Playbook in Football Investing

The investment criteria for sports teams is a clear value add play; find teams that are able to be acquired for cheaper, and grow them as quickly as possible. This is evident in previous acquisitions within football, especially within recent years where “mega deals” have been few and far between (acquisitions that include larger clubs). The major influx of capital from foreign investors, most notably from the United States, has majorly affected the overall market and has made football clubs a main prospect for value add investing with the firms that are willing to take on that investment. In 2025, there were a total of 76 transactions related to football clubs, with 55 of those emerging from foreign investors. Investors based in the United States accounted for 28 of those transactions, with England, Portugal, Italy, and Scotland the preferred destination for those investments.

Why the sudden shift in capital allocation? This is because of the clear path to success these teams have in terms of what needs to be done in order to grow. If you examine the clubs that were involved, notable investments include Heart of Midtholian FC in the Scottish Premiership, RCD Espanyol in Spain, and clubs in Italy such as AC Monza and Hellas Verona. You have probably never heard of these teams, however investors are purposely allocating capital to lesser known “cheaper” clubs, in which they can then invest in order to expand further. This could take years for the investment to materialize, or as short as 8 months. In the case of Hearts, their valuation has tripled in the span of one season with them being the leaders of the Scottish Premiership for the first time in 65 years. For Italian football, foreign investment has a clear motivation; target their underdeveloped infrastructure, strong global brand, and clear revenue gap in order to acquire a stake for lower valuation.

The broader market of investing vehicles such as private credit in football has rapidly expanded since the start of the COVID-19 pandemic, when clubs were unsure when revenue would return back to normal. Since then, a rising number of teams have utilized private credit and a wider variety of financial instruments to supplement lost revenue. Italian clubs as a whole, most notably Napoli, who were champions of the Serie A last season, earned well under €250 million in revenue, which is a fraction from other top European clubs in different leagues. This is similar to other clubs in Italy, who face major budget constraints while larger Spanish and English teams continue to thrive (Exhibit 2). Italian clubs in general are consistently struggling financially compared to large teams in other leagues, due to lower broadcasting revenues, outdated and publicly-owned stadiums that limit matchday income, a history of financial scandals, a weaker national economy, and less aggressive global marketing efforts. Collectively, these factors produce a league where revenue growth has failed to keep pace with wage inflation and competitive pressures.

Winning on the Pitch, Losing on the Books

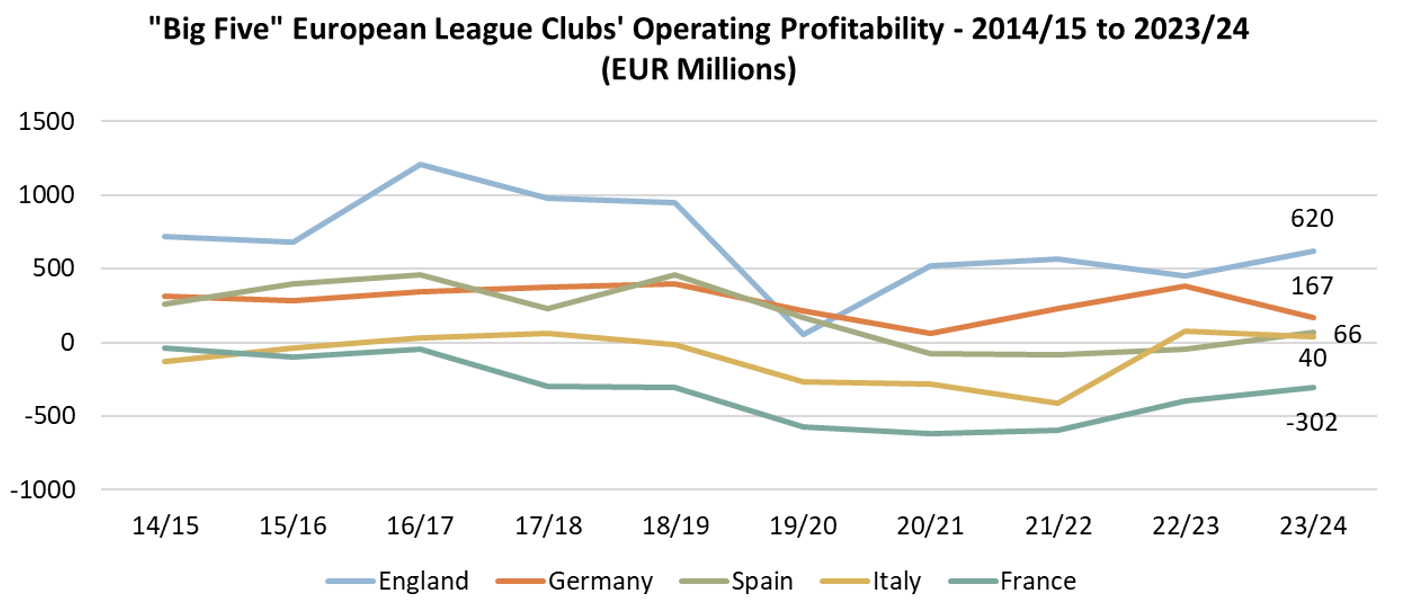

The primary challenge which confronts Serie A is not a temporary downturn or a sequence of isolated incidents, but rather consistent financial instability which has become structural across the overall league. Despite a high degree of performance in recent years from Serie A clubs, with Inter Milan reaching two out of the three Champions League Finals, domestic and European success has yet to bring financial stability for most if not all Serie A clubs. At the center of this instability is the shrinking gap between costs and revenues. In order to remain competitive with other European clubs, Serie A clubs have to match or be in the vicinity of wage bills, transfer fees, and broadcasting revenue. However, with difficulty managing the smaller amounts they receive from broadcasting revenue, the trend of overall instability has been incredibly difficult to break for most clubs.

Commercial monetization remains underdeveloped, and matchday income is constrained by outdated, publicly owned stadium infrastructure. The imbalance has made private debt a vehicle not for investment, but rather to support day to day operations. Overall, the financing vulnerability Serie A clubs face as a result sees them competing less consistently with clubs in other regions. Although clubs like Inter Milan have seen European success in the last three years, there are few other examples of Italian clubs remaining competitive on the largest stage, which is worrying for the broader league and fans alike. This instability is reinforced by incentive structures that reward short-term sporting success while deferring financial consequences.

Clubs are often pressured to prioritize immediate competitive performance over long-term financial planning, particularly in an environment where relegation or missed European qualification can trigger sharp revenue declines. As a result, financial discipline becomes reactive rather than preventative, entrenching a cycle in which clubs require continuous capital support simply to maintain competitiveness rather than to invest in sustainable growth.

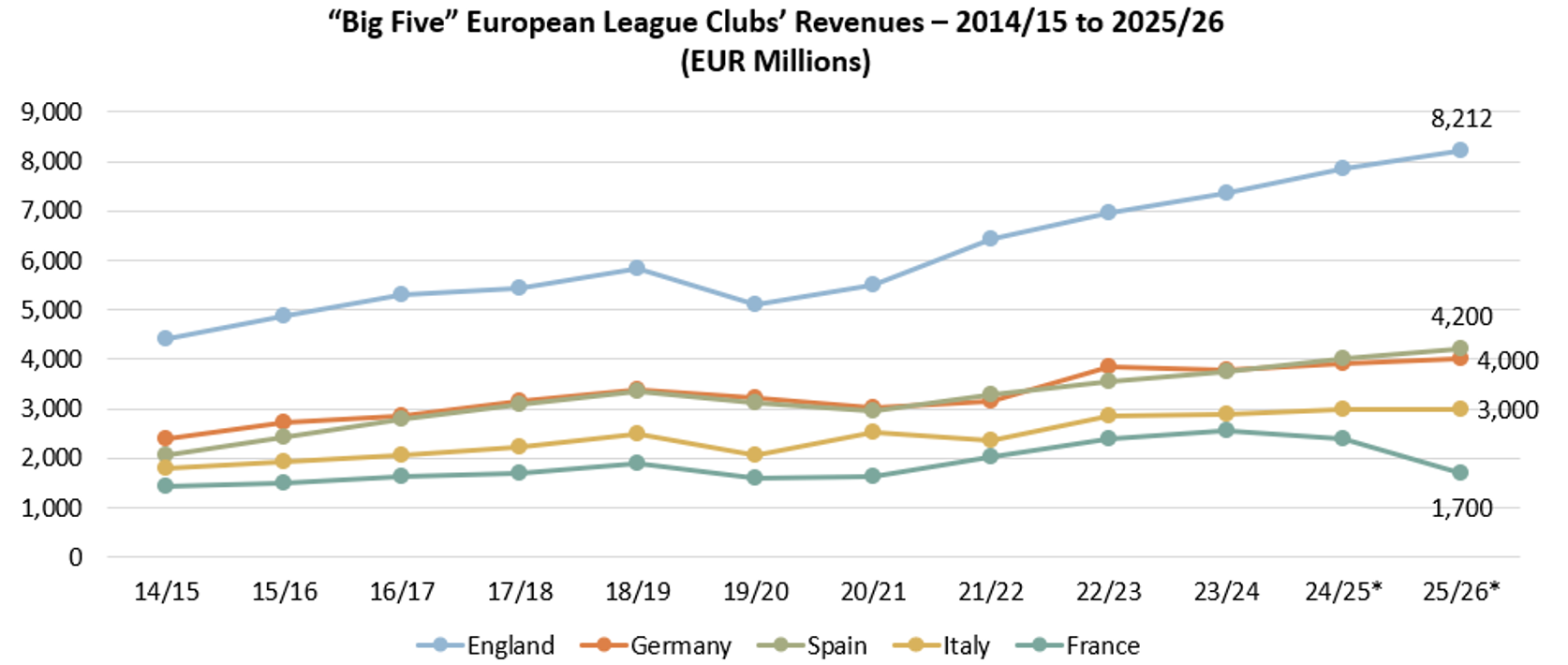

So in hindsight, Serie A teams should be performing well financially, especially due to the fact that teams such as Inter Milan have reached two out of the last three champions league finals, netting €137 million from the competition in the 2024/2025 season. However, this is not an issue of performance. Within any sport, teams that rely on performances in order to cover costs financially have historically not done well especially when those performances were missed out on. Leeds United in the early 2000s, Rangers F.C. in 2012, and most notably larger Italian clubs like Fiorentina and Parma Calcio in the early 1990s all fell victim to this strategy. The payments received by Inter Milan and other Italian clubs can be seen more as a “bonus layer” rather than that of additional revenue. This is somewhat due to how revenue in Italian football has grown relative to other top 5 leagues since the late 1990s (Exhibit 3).

In the 1996/1997 season, Italian football was second in terms of revenue in the top 5 leagues, with a moderate gap to the Premier League which has been a consistent leader. Fast forward to the present, Italian football sits fourth on the revenue scale, and projected to be outpaced by about €1 billion by the Bundesliga and La Liga by the end of this season. Bundesliga clubs are expected to generate a projected total of €4 billion this season, with 14 percent coming from matchday revenues (ticket sales, concessions, etc.), 40 percent broadcasting, and 46 percent commercial revenue. Italian clubs are expected to generate €3 billion this season, with little to no growth from last year and being outpaced by leagues like the Bundesliga in all portions of main club revenue, those being matchday, broadcasting, and commercial. This makes it a top priority for Italian clubs as a whole to diversify their income streams and look to other clubs in different geographies in an effort to grow their revenue base regardless of on pitch performance.

Representative Cases

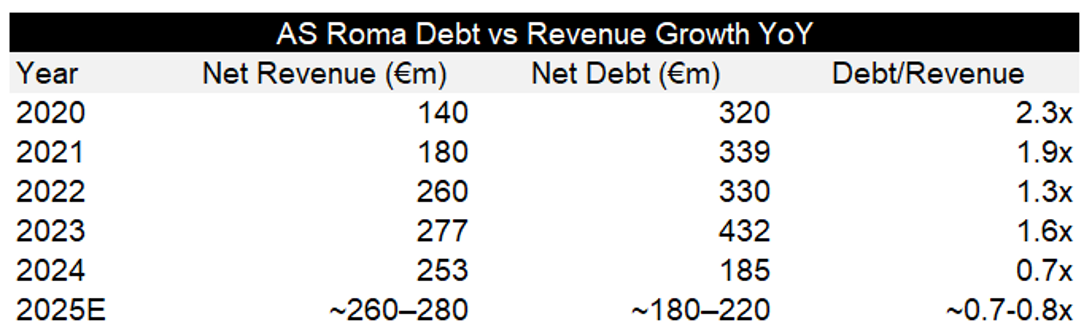

AS Roma has been one the clubs involved in debt financing and more recently repaid €275 million worth of bonds in an effort to take on new debt. This however, is still overshadowed by the continuous losses the club has incurred, majorly affecting their ability to compete on and off the pitch. On top of that, previous ownership had undergone major financial mismanagement, and exhausted most traditional financing options including listing the club as a public corporation in Italy. It was delisted in 2022 after The Friedkin Group took over the club, but this is just one of the major highlights of previous mismanagement of a club valued so highly among fans. Although improvement has been shown through cutting transfer spending, reducing staff, and relying on academy players, the debt in which the club is taking on currently is not tied to any future revenue, making it difficult for the club to grow past the significant deficit previous ownership has built up. In recent years, the mismanagement of the past has caused AS Roma and other Serie A clubs to fall victim to capital requirements made by the FFP (Financial Fair Play, governing body of finance for European football).

In 2025, AS Roma were ordered to come up with €90 million, which needs to be raised in capital gain. In order to do so however, they must rely on performance improvements as well as player sales that may or may not materialize, raising serious red flags in terms of overall structure. Over the past 5 years, the gap between Roma’s debt versus revenue growth has seen an alarming disparity, which initially raised concern for the club and FFP (Exhibit 4). Capital deployment into the correct areas for revenue growth has become non-existent for the club, having to scrape by cutting operating expenses when revenue targets are drastically missed. The silver lining is despite this, club performance has seen a minimal drop, which has given fan morale and their bottom line a much needed boost.

By contrast, Tottenham Hotspur, a Premier League club, illustrates a more disciplined approach, having taken on significant leverage to finance a new stadium explicitly designed to expand long-term revenue through premium hospitality, non-matchday events, and commercial partnerships. While Roma’s prior ownership exhausted traditional financing avenues, including a public listing later reversed under The Friedkin Group, Tottenham’s debt was deployed as growth capital rather than loss coverage. Tottenham’s new stadium construction, although unrealistic for clubs in denser populations such as Roma, generated over £100 million in matchday revenue alone during the 2023-2024 season. The project cost close to £1.2 billion however is expected to gross well over £100 million in additional revenue per season, making it an incredibly worthwhile investment with an estimated IRR between 6-10 percent.

The comparison between AS Roma and Tottenham Hotspur can be said to serve the function of a case study in capital allocation strategy, where the former’s refinancing can be viewed as an exercise in debt cycling to address liquidity issues, while the latter’s long-term project financing is directly related to revenue generated from the stadium. The stadium of Tottenham Hotspur was designed to be a versatile commercial entity that could accommodate NFL games, concerts, and corporate events throughout the year, not just domestic league matches.

From Survival to Strategy: Rewiring Serie A’s Financial Model

Implementing a similar structure would allow Serie A clubs to secure immediate funding while aligning repayment obligations with future revenue streams, rather than fixed interest payments. This approach reduces the burden of current debt servicing, creates long-term sustainability, and positions the club to rebuild competitiveness without compounding financial instability. An example of this is a deal with FC Barcelona involving the American investment firm Sixth Street. In order to offset recent losses, FC Barcelona accepted an approximately €667 million revenue linked loan structure for a percentage of television rights received from their domestic league.

Initially, in June of 2022, Sixth Street acquired 10% of FC Barcelona’s domestic TV rights for the next 25 years for €207.5 million (club described a €267 million “capital gain”). By the end of July, Sixth Street had acquired an additional 15% for a total of 25%, for the total price listed above. The popularized term related to the club has been employing “economic levers” in order to register new players and improve financial liquidity. However, this capital injection has not only been used to cover immediate costs. A large portion of this capital has been invested into the redevelopment of the Camp Nou, their stadium, which will bring additional revenue to the club. On top of that, the club has introduced many other revenue streams such as digital content, expansion of merchandising stores within Spain, and introduction of special PSL tickets (30-year season tickets) which has brought in millions of needed revenue. Since these changes, the club's financials have seen a complete turnaround since 2020 when they were at heavy risk of bankruptcy with rumours of a forced sale circulating. What Italian football can take from this is first, to be optimistic regarding revenue diversification strategies with how fast they could, and second, in order to utilize debt effectively a portion of that debt must be allocated to revenue growth strategies.

Modernization of stadiums should be the main pillar of this strategy. When compared to other Premier League clubs, Serie A clubs are lagging behind in having control over stadiums and, therefore, monetizing non-matchday revenue. The modernization strategy of Tottenham Hotspur Football Club is an example of how leverage can be used to generate diversified revenue streams throughout the year. Serie A clubs should partner with infrastructure investors to raise funds for purchasing and building stadiums or additional infrastructure to support existing complexes.

In Italy however, the main shortfall for expansion is the multi-layered approval system that is required in order to put through expansions like ones for stadiums and entertainment complexes around the country. The typical timeline for an expansion or new stadium construction in England is typically between 2-4 years while in Italy it can take between 5-8 years. This means that projects will have to be planned and started well in advance to meet similar timelines. In cities such as Rome, where multiple teams such as Lazio and Roma play, there are cultural ruins under almost every square kilometre of land that stops construction numerous times, making it increasingly difficult to improve infrastructure in general. To mitigate this risk, surveying groups have been called in for when infrastructure must be built or renovated, however there still exists multiple regulatory hoops that make construction extended compared to their English counterparts. Although an infrastructure expansion would take longer, the opportunities remain the same.

Viewing the Tottenham model, they gain additional revenue through non-matchday events, visitor attraction, naming rights, as well as district real-estate where applicable. Although these are not feasible for all Serie A clubs, an investment in infrastructure is still proven to bring added revenue through some or all of these avenues. We have seen this model applied through some Serie A clubs already. Como has been a staple in value-add investing for the Hartono Brothers who acquired the club in 2018. They have since climbed from Serie D (the fourth division of Italian football) to now Serie A (the first division) and are expected to finish in the Top 4 this season, qualifying for Europe. Their new stadium expansion is expected to add 20,000 seats as well as a “365-day model”, incorporating retail, hospitality, and non-matchday events. The total expansion cost is expected to be around €30 million to €40 million, however revenues are very likely to exceed expectations due to the international tourism increase related to the club and surrounding area. Other clubs should utilize these investments in particular as a blueprint for improvement. Although some may not have the international tourism that the city of Como has, they can still utilize this model in order to rely less on club performance and more on recurring guaranteed revenue to get finances in order.

It is imperative that there is a change in the way Serie A is being managed. Incentives are being given to Serie A clubs to achieve sporting success, which is affecting them negatively in the long term. Financial control and commercialization of Serie A should be improved to reduce the structural difference in revenue generated by Serie A clubs when compared to other European clubs. Serie A’s revival will not be achieved by competing with other European clubs regarding wages; it will be achieved by developing a financial system where debts are used to fund growth, infrastructure is used to generate revenue, and sporting success is achieved through stability and not constant borrowing. Models utilized by other leagues can be applied and have worked in the past. LaLiga in Spain utilizes a wage model in which allowable squad costs for the following season are constrained by projected revenue with minimal exceptions. This is a pro-active approach that allows wage costs to be kept under control league wide. The average Serie A club today earns €145 million in revenue, however the average wage bill is €98 million. Although there are outliers for the larger and smaller teams, it is still worrying that around €47 million per club is supposed to be utilized for all other expenses while still maintaining a profit. Performance volatility as a whole leaks heavily into domestic profit and loss figures, particularly that of European tournament performance. Although this is apparent in most top leagues, mitigating this volatility through implementation of more financial controls such as the wage bill constraint can drastically help clubs grow at a stable and sustainable pace while aiding the overall league model.

What is Next for Serie A

Serie A is currently undergoing a major growth problem in comparison to other top leagues. In the early 2000s, their overall revenue was second only to the Premier League, while it has now been overtaken by both La Liga and the Bundesliga. We have seen implementation of incredibly lucrative investments with clubs like Como, however in order for the league to be as prosperous as it previously was, these structures must be utilized league-wide on a consistent basis. The current issue that Serie A is facing has nothing to do with lack of talent, history or global appeal. But rather a string of poor structural decisions made by governing bodies and the clubs themselves. The future of Serie A will ultimately rely on their ability to change and embrace systematic reform on multiple levels. If Serie A can address these changes effectively, it can pave the way to a larger global football giant.

Exhibit 1

Exhibit 2

Exhibit 3

Exhibit 4