Value Village: Fixing the Price–Value Gap

By: Edward Gordon

The Ivey Business Review is a student publication conceived, designed and managed by Honors Business Administration students at the Ivey Business School.

Value Village: Fixing the Price–Value Gap

Value Village (“VV”), also operating as Savers and Village des Valeurs, is the largest for-profit thrift retailer in the U.S. and Canada, holding ~64% of the North American for-profit thrift market. Its business model has three main pillars: sourcing, resale, and recycling. First, sourcing: ~35% of VV’s supply is purchased from nonprofit partners, who are compensated at a set rate per pound of donations collected to support their missions, with the remaining inventory coming from on-site donations. Second, resale: items are sorted, priced, and sold for profit across more than 300 stores in North America and Australia. Third, recycling: unsold goods are redirected through large-scale reuse and recycling programs, diverting ~700 million pounds of clothing and household items from landfills each year.

Problem: Consumers Are Paying Too Much for What They Get

For decades, VV has relied on a simple proposition: shoppers trade certainty for discovery in exchange for meaningful savings. That trade-off is now under strain. As used goods are increasingly priced close to—or sometimes above—new retail alternatives, customers are beginning to question the fairness and logic of VV’s pricing model.

Aggressive pricing practices at VV have increasingly led to a decline in perceived customer value. A comparison published by CBC between new goods sold at Dollarama and Walmart and equivalent used goods priced at VV sparked backlash; for example, a customer spotted a used Dollarama vase in Toronto with a Value Village price tag of $8.99, three times what it would have cost new. Similar concerns are echoed across online forums such as Reddit and in customer reviews on Google Maps.

To contextualize the impact of the erosion, comparable store sales, which measure year-over-year growth at existing stores, serve as a key demand indicator. Canada comps were approximately +5% in 2023 but declined to –4% in 2024 before partially recovering to around +2% in 2025. While perceived value is not the sole driver of these fluctuations, the transaction-led decline suggests sensitivity among value-conscious customers, making value perception critical to stabilizing long-term growth. At its core, the tension lies between two sides of the value equation: the perceived value consumers receive from second-hand goods versus the price they are asked to pay. Solving this tension will require addressing both sides of that equation through the primary causal factor of sourcing constraints that limit product consistency.

Causal Factor: Supply Constraints & Product Quality

VV’s reliance on donated goods as its primary source of inventory has contributed to inconsistent product quality and a limited assortment, pushing the price-value tension. Under the current sourcing model, constraints manifest in several ways. First, donation volumes and quality fluctuate significantly, exposing stores to disruptions when supply declines or skews toward lower-quality items. Second, donated inventory requires labour-intensive processing, including sorting and pricing, which creates operational bottlenecks during periods of strong consumer demand. Third, after going public in 2023, management noted that VV’s low average item price of ~$5 makes online sales difficult once shipping and fulfillment costs are included. As competition intensifies and consumer trust in value erodes, these supply-side limitations increasingly constrain VV’s ability to justify higher prices through product quality or consistency. Restoring perceived value may require not only changes in pricing behaviour, but a reconsideration of how inventory is sourced, particularly through channels that provide greater control over assortment while leveraging VV’s existing scale and distribution network.

Opportunity: Liquidation Sourcing Expansion

One potential opportunity lies in expanding sourcing channels to include returned merchandise from large retailers such as Amazon and Costco. Currently, a significant share of refunded goods is sold through liquidation and auction platforms, where inventory is typically purchased by smaller resellers with limited scale and distribution reach. VV's national store footprint and capacity for bulk purchasing could offer these retailers a more attractive recovery rate than fragmented, smaller resellers, making VV a compelling alternative buyer. Introducing a secondary supply stream of returned goods could directly address the price–value tension faced by VV customers by improving product quality and perceived deal value. Unlike donated inventory, returned merchandise often includes lightly used or open-box items with higher resale potential, offering customers clearer value through savings mapped directly against current retail prices.

VV is uniquely positioned to unlock this sourcing channel at scale. Equity analysts often benchmark VV against clothing resale platforms such as The RealReal, a luxury consignment marketplace, and ThredUp, an online thrift and resale platform. However, liquidation-sourced inventory extends well beyond apparel into categories such as small appliances, home goods, seasonal products, and electronics, areas where many resale competitors struggle to operate consistently due to the testing, verification, and quality control demands these categories require. While labour intensity varies significantly by category, VV's existing infrastructure and trained grading workforce mean it is better positioned than competitors to absorb these requirements, making category selection a question of fit rather than feasibility. Liquidation sourcing typically requires bulk purchasing, a structure that already aligns with VV’s current sourcing model. With its national store footprint and established logistics infrastructure, VV is well-positioned to compete in this segment; its scale and distribution capabilities could allow it to outperform smaller liquidation outlets while improving inventory consistency and perceived value for customers.

VV should consider several approaches when expanding into liquidation:

1. Limited-SKU, High-Volume Liquidation Strategy

Apparel should be the first category if VV expands into liquidation, as it represents ~65% of current merchandise sales and carries lower operational risk than categories like electronics, which require testing and pose greater reputational risk if defective. One potential approach is entering online “new” apparel, meaning overstock or shelf pulls sourced from brands or retailers.

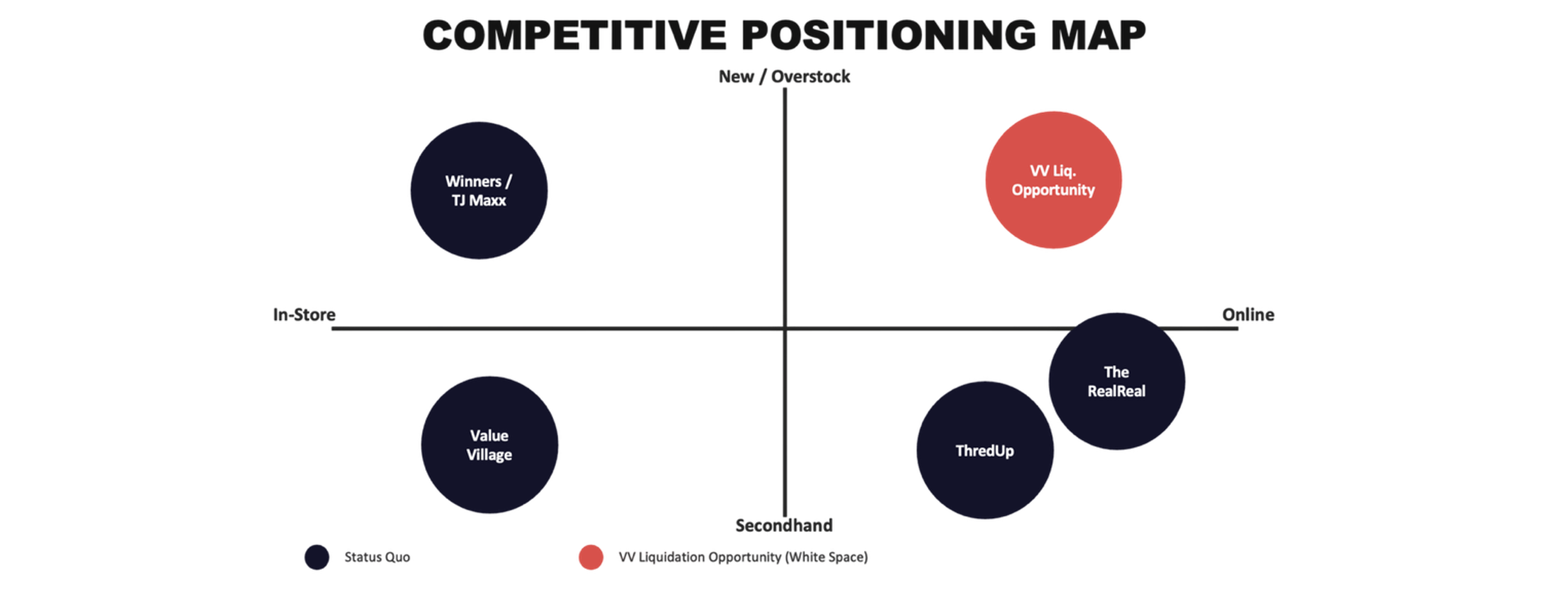

Mapping competitors by product condition (Figure 1), new vs. secondhand, and channel, online vs. offline, reveals clear clusters: off-price retailers like Winners and TJ Maxx sell “new” overstock primarily in-store, and have struggled to extend that model online due to high SKU variety and rapid inventory turnover. Platforms like The RealReal and ThredUp focus on online secondhand. VV currently operates in the offline secondhand space.

Figure 1: Value Village Competitive Positioning Map

Rather than broadly competing with them, VV should selectively source limited, high-volume liquidation items, such as overstock basics or repeatable seasonal goods. As the first liquidation category, focusing on predictable items with high volumes would reduce variability and increase average item value without requiring a full shift into traditional off-price retail.

2. Online Channel Rationale

Beyond the sourcing opportunity, liquidation inventory also creates a viable path for VV to finally establish an online presence, a channel VV has itself identified as a strategic vulnerability, explicitly flagging its status as a "brick and mortar" only retailer as a risk factor in its filings. Goodwill's experience illustrates what is possible. ShopGoodwill.com generated ~$450 million in merchandise value in 2025, up 22% year-over-year, its best performance in 26 years. The barrier, as previously noted, has been unit economics: VV's ~$5 average item price makes online fulfilment cost-prohibitive at scale. Liquidation-sourced inventory directly resolves this. Critically, this does not require changing what happens in physical stores. VV's customer base naturally segments across channels: thrill-seekers who value the discovery experience continue shopping in-store as before for donated goods; value-focused shoppers can browse liquidation goods online with more pricing transparency and less variability; and flippers, which are buyers hunting for underpriced branded or high-demand items to resell, represent an incremental online audience, gaining access to VV's inventory nationwide rather than being limited to their local store, allowing them to find the best deals for their needs. An online B2C channel, therefore, expands VV's addressable market rather than cannibalizing it, while operating in largely uncontested territory that off-price retailers have not cracked at scale.

3. Higher-Value Category Expansion

Diversifying into higher-value categories could improve margins and make online presence more viable. Beyond apparel, VV could expand into categories such as branded toys and seasonal items, such as outdoor gear with repeatable demand, home textiles and soft home goods, such as sheets, towels, and décor, and kitchenware. These products typically sell at higher prices than books or miscellaneous hard goods, while remaining easy to ship and low in defect risk compared to electronics. They also align well with VV's largest customer groups: value-conscious families and younger shoppers, including Gen Z consumers furnishing their first homes or dorms. A higher average item price does not mean worse value for customers; it means better items at the same deep discounts. Unlike donated goods, liquidation inventory often consists of new or lightly used items, reducing the uncertainty customers currently accept in exchange for savings. With retailers recovering as low as 15% of an item's original retail value through liquidation channels, VV could pass meaningful savings on to shoppers while maintaining its own profitability. More immediately, a higher average item gives VV a viable entry point to build its online presence before pursuing broader digital expansion consistent with its long-term positioning.

4. Build vs. Buy Considerations When Expanding into Liquidation

When expanding into liquidation sourcing, VV should pursue an organic build rather than an acquisition. The case for building rests on VV's existing infrastructure: its ~24,000-person workforce, processing centers, and established bulk purchasing relationships already provide the operational foundation for a liquidation channel. VV is a more attractive recovery partner for major retailers than the fragmented small resellers that currently dominate liquidation buying. That scale advantage, combined with a national store footprint that offers retailers predictable volume and geographic distribution, gives VV the standing to approach Amazon, Costco, and comparable retailers directly without intermediary platforms.

Conversely, an acquisition strategy offers limited value for VV’s specific retail needs. Scaled platforms such as B-Stock maintain long-standing relationships with major retailers including Costco and Samsung, and both B-Stock and VV are majority-owned by private equity firms, creating a potential ownership transition scenario that Ares, as VV's sponsor, could explore. However, B-Stock operates as a B2B auction intermediary, whereas VV needs a direct B2C retail channel; acquiring it would bring retailer relationships but not the consumer-facing model VV actually requires. A more targeted path would be acquiring a smaller regional liquidation operator as a proof-of-concept before scaling organically across VV's full network.

The Unsorted Pile – Risks and Mitigations

Liquidation Sourcing Expansion

Adding a liquidation sourcing channel raises a practical concern of inventory overstocking: VV currently turns its inventory more than 15 times a year, according to its 2024 annual report, meaning that existing supply is well-matched to demand. Layering in liquidation volume without adjusting current sourcing could overwhelm the sales floor faster than the stores can clear it.

The most straightforward lever here is scaling back purchases from nonprofit partners, who currently account for ~35% of VV's supply. VV pays these partners by the pound, meaning reduced volumes would create room for liquidation inventory without an overall supply surplus. However, pulling back from relationships with nonprofits is risky and may damage VV’s community goodwill and corporate identity. Moreover, on-site donations, by contrast, cost VV far less to acquire, primarily the labour to process them and a discount coupon handed to donors, so those should remain untouched; cutting them would sacrifice low-cost supply while also visibly diminishing the in-store donation experience that drives foot traffic.

As such, a solution for inventory that still doesn't move after several weeks on the floor is for VV to introduce a blind box clearance format, bundling unsold items by category, such as ten pieces of athletic wear or a set of kitchen items, at a fixed discount price. The key to making this work without eroding trust is curation: each bundle needs to include at least a couple of appealing items, so shoppers feel the gamble was worth it rather than feeling offloaded on. If done well, this turns a markdown problem into a minor treasure hunt of its own, consistent with VV's broader brand experience while recovering value on slow-moving stock.

Do Savers Value the Treasure or the Hunt?

Limiting SKUs and introducing more structured liquidation inventory may enhance price certainty and raise average item value, but it could also alter the core thrift experience. VV’s appeal has traditionally rested on the “treasure hunt” dynamic where unpredictability is part of the value proposition and consumers accept variability in exchange for potential savings. A more curated or predictable assortment, particularly online, reduces that uncertainty. However, the proposed expansion addresses this directly: by routing higher-value goods online but still integrating high-volume overstock onto the physical sales floor, VV preserves the discovery-driven treasure hunt for shoppers who value it, while opening a distinct channel for value-focused shoppers who prioritize price certainty over variety, and for flippers seeking underpriced branded items to resell. Each segment is served on its own terms, without one cannibalizing the other.

Regardless of the expansion path VV chooses, the core objective remains improving perceived value, and sustaining perceived value requires improving the underlying economic offering. Selective expansion into liquidation categories could broaden product selection and allow consumers to purchase new or overstock items at meaningful discounts, raising average basket prices for e-commerce viability while also offering more guaranteed quality for customers. A stronger merchandise mix would thus reinforce both the psychological and financial dimensions of value for savers, supporting the village in achieving more stable demand and long-term growth.

Editor(s): Emily Cao

Researcher(s): Nancy Huang